Recently, concerns have been raised on several occasions that the Green transition has been – if not cancelled – at least postponed. The UN climate conference in the spring was a disappointment for many. The United States has announced that it will withdraw from the Paris climate agreement. Finland has also reduced its obligation to distribute transport fuels.

And what about shipping? Shipping has, perhaps surprisingly, increasingly tightened its goals to abandon fossil fuels. According to a IMO decision made in April 2025, shipping is the first sector to have set a globally binding economic instrument aimed at reducing greenhouse gas emissions.

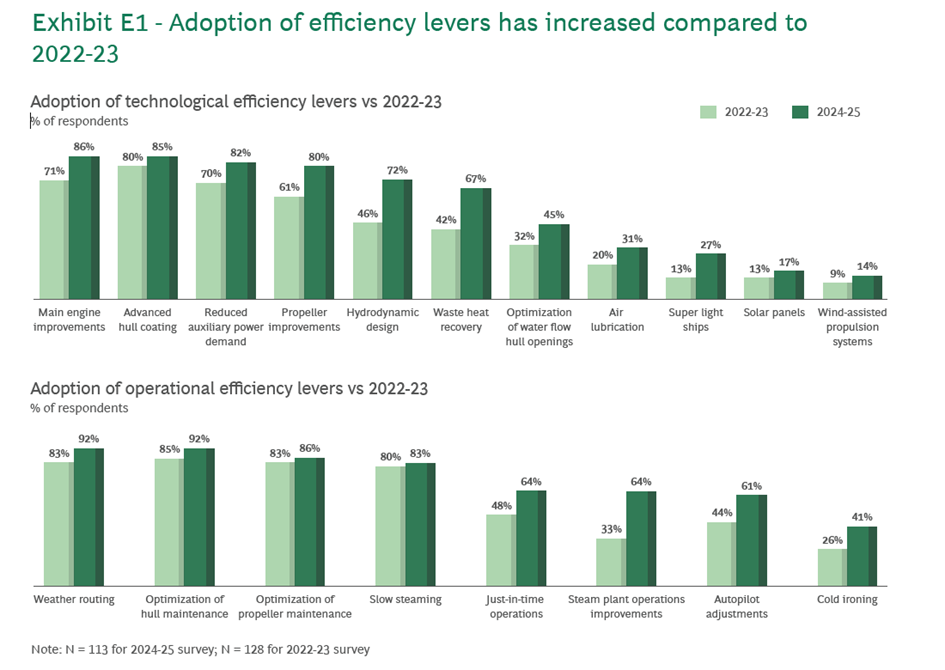

This spring, an interesting study by the Boston Consulting Group (Kuttan et al. 2025) was published, which examined the attitudes of maritime operators towards abandoning fossil fuels. The study analyzed 114 shipping companies or operators. The respondents included all types of shipping companies, from tankers to small tonnage, of all sizes (measured by number of ships and balance sheet value) and from all over the world.

The survey classified respondents into three categories: Frontrunners, Followers and Conservatives, based on how they have implemented low-carbon solutions. Frontrunners set a goal of carbon neutrality. Followers are more moderate in their low-carbon goals. Conservatives are only just starting their path towards carbon neutrality.

The survey found that more than half of container shipping companies were Frontrunners, as were most of the large shipping companies. However, it was evident across all groups that both technological and operational measures to reduce fuel consumption have become more common compared to the survey conducted a year earlier (see Figure 1). The use of alternative fuels has also increased across all groups. LNG (even though it is a fossil fuel) and bio-based fuels are still considered more common alternative fuels.

Of particular interest in the report, however, was how differently Frontrunners, Followers and Conservatives see their challenges on the path to low emissions. It was still unclear to Conservatives what kind of solutions exist to reduce greenhouse gas emissions and how they work. For the Followers, the solutions were already clear, but they are still comparing the available options with each other, while for the Frontrunners, the solutions and their functionality are already familiar, but financing the investments is a concern.

For Conservatives, biofuels were the most popular alternative fuel, while for the Followers and Frontrunners, it was already clear that biofuels cannot be a long-term general solution for shipping. Their attention is focused on ammonia and methanol. Although none of the shipping companies surveyed have ammonia-powered ships, methanol is already used by six percent – all Frontrunners.

Figure 1. Adoption of the use of maritime efficiency measures in the interviewed companies (source: Kuttan et al. 2025)

Perspectives on the Baltic Sea

Although the results of the above report are encouraging, there are several differences in the discussion in the Baltic Sea region. From the Baltic Sea perspective, it is surprising that LNG is still included in alternative fuels, even though its life-cycle emissions may even exceed those of traditional diesel. Equally surprising is the absence of battery electricity among the fuel options.

In particular, the following questions are currently being considered by shipping companies in the Baltic Sea:

1. The complexity of the regulations and the possible overlap of EU and IMO regulations. Each shipping company is different, and the measures to achieve low emissions are different. I recommend carefully calculating the effects on both actual emissions and regulatory requirements. As an example, in particular, the opportunities provided by pooling and the compliance of emission reduction measures on requirements of regulations.

2. Supply of alternative fuels. It is likely that there will be a shortage of biofuels – unless there is an own or otherwise assured production plant, biofuels are unlikely to be a solution for shipping companies. Instead, electricity, hydrogen, ammonia and methanol are certainly each part of the fuel palette of the future.

3. Risks. Is it worth being a pioneer if the chosen technology turns out to be a bad solution in the future? There are many examples from history, for example, emissions during the life cycle of LNG, toxic residues of sulfur scrubbers and of course countless technologies that have failed to function as intended.

The requirements of environmental regulation and understanding existing technology require special expertise in shipping companies. It is important to develop the company’s own expertise and to cooperate so that information on best and worst practices can be shared.

Why is the shipping industry a pioneer?

Many of us are probably wondering how the shipping industry – which has traditionally been considered as conservative – has thus actively started the transition towards carbon neutrality. I personally see two reasons behind it.

Firstly, shipping started from a backward point of view compared to other modes of transport. Before the adoption of the Sulphur Directive, very cheap but highly polluting heavy fuel oil was used in maritime transport. Little attention was paid to fuel consumption – shipping companies made savings and sought additional income even by means that increased consumption.

When the Sulphur Directive started to pay attention to fuel consumption (see the measures in Figure 1), results were quickly seen. My research colleagues from other fields of transportation do not want to believe their ears when I tell them that the latest generation of ships consume up to half as much fuel as those of twenty years ago. This has naturally given the green transition a positive reputation in the industry.

The second reason is perhaps the traditional risk-taking and – shall I say – greed of shipping. Although today the Baltic Sea shipping companies are stable and responsible, in the past people went to sea, attracted by the lure of better earnings, often taking great risks – to fish ever further, to conquer colonies or to import expensive products from distant lands.

Even today, we see many features in shipping that are considered forbidden in other industries – such as tax evasion by flying ships under flags of convenience, salary payment based on a person’s background or cartels, commonly called conferences in this industry. The so-called shadow fleet ships are particularly problematic.

Pioneering shipping companies see the green transition in shipping as a new and acceptable opportunity for risk-taking and higher profits, if they can reduce their emissions and the costs of regulations more effectively than their competitors.

Source:

Kuttan, S. C., Veeraraghavan, A., Sivaprasad, Khaing, C. and Le Tan, J.: Advancing Maritime Decarbonization: Insights from the GCMD-BCG Global Maritime Decarbonization Survey (2nd edition), June 2025.

This article was previously published in Finnish in Navigator Magazine, an online magazine for maritime professionals, on 27 June 2025.