Background

Russia started a war against Ukraine in February 2022. Russia largely finances its war by selling fossil fuels abroad, especially crude oil. The G7 countries want make to Russia’s military actions difficult, but at the same time they fear that oil sale restrictions will significantly increase the price of oil and thus hinder the growth of countries dependent on Russian oil and the world economy.

In December 2022, Western countries, including the G7 countries and the European Union, imposed a cap in an attempt to limit Russia’s revenue stream from oil sales. Hence, they have imposed a ban on transporting oil whose price is more than 60 dollars per barrel. For this, they try to ensure that the oil bought from Russia should be cheaper than this, and thus Russia would not get too much income from the sale of oil, and at the same time the oil would still flow to the world and for use.

Russian oil is transported both by tankers and by pipelines. At sea, in response to this sanctioning of the transportation of Russian oil, certain tankers have appeared to carry precisely this sanctioned oil cargo. These ships are called the shadow fleet, because there is no accurate information about their condition, insurance and whether they comply with sanctions regulations. A large part of this Russian seaborne oil export goes through the Gulf of Finland, but also from the Black Sea and the Far East. Part of the transport is also a so-called STS operation (Ship-to-Ship transfer), where the oil coming from Russia is transferred at sea to another ship, and thus an attempt is made to destroy the information about the origin of the oil.

Shadow Fleet

Currently, it is estimated that at least 400, but depending on the source, even more than 1,000 tankers are currently transporting this Russian oil, which costs more than $60 per barrel, i.e. as part of the shadow fleet.

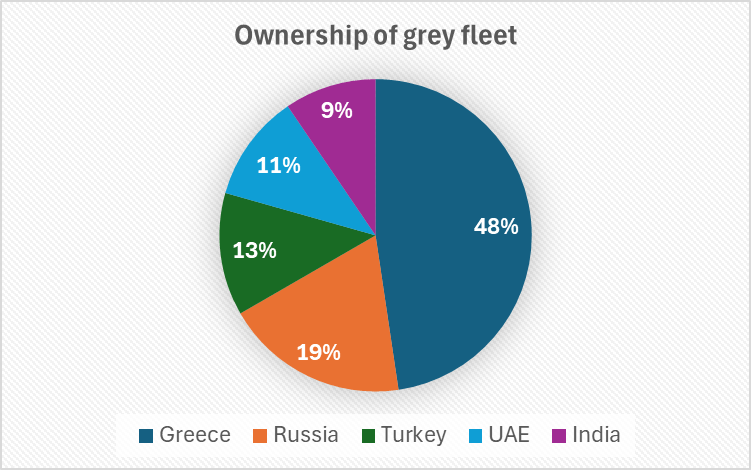

Figure 1. Ownership of the Shadow Fleet (source: https://windward.ai/knowledge-base/illuminating-russias-shadow-fleet/ )

Shadow fleet vessels are practically like any tankers that have transported oil on the world market in the past, but now they carry this sanctioned cargo. Their special feature is that they quickly change owners and flag states, but above all their insurance arrangements are unclear.

The ownership of the shadow fleet is largely located in the same countries as where the traditional tonnage operates, large owners are, for example, Greece, but there is also Russian and Turkish ownership.

Every merchant ship that sails the sea is flagged to a country. It means that it complies with the legislation of the country in question and the country in question is obliged to monitor that the ship meets international safety and other regulations. At the same time, the flag state can collect tax from its ships. Flag states carry out so-called flag state controls on their ships.

In principle, the merchant fleet’s choice of flag state is not limited in any way, i.e. shipping companies are allowed to flag their ships under the flag of any country they want. This has led to a competition in which many small countries, such as Liberia, Panama or the Marshall Islands, have attracted a large number of ships owned elsewhere under their own flag. The attraction takes place, for example, with low taxation. Often these countries of convenience are also more lax in their inspections than other countries. For example, a large number of ships owned by the United States are flagged to Panama, and Greek ships can also be found in the registers of many other countries.

However, a bigger problem than flag state and ownership is ship insurance. All ships traveling at sea must be insured by the maritime industry’s own insurance institutions. Insurance institutions carry out their own inspections of ships and make sure that there are no ships at sea with a high risk of accidents. There is no information about the shadow fleet’s insurance, or the ships are insured with, for example, Russian marine insurance institutions, whose operation is uncertain. Ships may be in poor condition.

The demand for ship capacity affects the condition of the ships

In the shipping market, one important factor is the number of ships. There are only about 100,000 ships registered as merchant ships in the world. Of the combined capacity of these ships, just under a third are tankers. When the world is in an economic boom period, the amount of shipping increases considerably. The amount of free ship capacity decreases and the price of sea transport increases. Correspondingly, during the low season, the amount of goods transported decreases, fewer ships are needed, and sea transport prices fall.

Figure 2. Dynamics of the maritime market

It should be noted that during the boom period, when more ships are needed, ship scrapping is delayed, and then there are more and more ships in poor condition in traffic. During the recession, the amount of ship capacity decreases, because more ships are taken for scrapping.

When Russia started a war against Ukraine, several European countries stopped buying Russian oil. New customers for Russian oil were found in India and China, among others. The average sea transportat of crude oil became significantly longer, so that in order for Russia to be able to export the same amount or even more oil to finance its war, significantly more ships around the world were needed to transport the same amount of oil.

Because of this, there is currently a greater need for oil-carrying ships than before, and their average age has increased. Fewer ships are taken to the scrap yard.

The shadow fleet’s risk to the environment

Since the ships of the shadow fleet are older than average, they also have a higher risk of accidents. The average age of shadow fleet tankers has been calculated to be a little under 20 years. A tanker over 20 years old is considered old. Engines or steering systems of an old ships can fail, in which case there is a risk of deviating from fairways that can lead to an accident. Over time, an accident at sea can also occur from iron fatigue.

When the Soviet Union collapsed more than three decades ago, a large part of its Baltic Sea ports remained in the independent Baltic countries. At first, Russia continued to export its oil and other export products through other countries as transit. Finland also acted as a transit country, although mainly for the import of Western goods. Gradually, Russia got its own ports built in the bottom of the Gulf of Finland, such as the expansions of the port of St. Petersburg, the port of Koivisto, the port of Uura, etc. At the same time, transit transport through Finland and the Baltics has decreased.

Tanker traffic has increased considerably in the Gulf of Finland over the past thirty years. At the same time, constant attention has been paid to the risk they cause. One of the most significant measures to improve maritime safety in the Gulf of Finland and prevent oil accidents has been the so-called GOFREP system (Gulf of Finland Reporting System). It means that every merchant ship arriving in the Gulf of Finland registers with the Finnish, Estonian or Russian maritime surveillance or VTS-center and tells where it is heading. The vessel is monitored, and if it turns out that the vessel deviates from the route, it is contacted and advised of the correct route.

Russia’s crude oil production as a whole is more than 10 million barrels per day. More was produced in the late 1980s, but production fell to around 6 million barrels in the early 1990s. About a third of Russia’s seaborne oil exports go through the ports of the bottom of the Gulf of Finland, i.e. Primorsk (Koivoston), Ust-Luga (Laukaansuu), St. Petersburg, Vyborg and Vysotsk (Uura). Primorsk and Ust-Luga are the largest ports, with a total of about 1.5 million barrels per day passing through them.

The security measures have been successful. The Finnish VTS Center announces every year that a dozen potential accidents have been prevented with the GOFREP system. Shadow ships also comply with the GOFREP system, and they also report to VTS centers when they arrive in the Gulf of Finland.

Another significant way to reduce the risk of major oil accidents has been the requirement that tankers must have a double bottom. Already in the early 1990s, the international maritime organization IMO decided that all new tankers carrying more than 5,000 tons must be equipped with a double bottom. So if the ship runs aground, in the best case, only the outer bottom will be damaged and the oil will not spill into the sea.

It should also be remembered that the value of a large tanker’s cargo can be up to two hundred million euros. In commercial shipping, the owner of the cargo naturally wants to keep his cargo safe, to have the cargo sold and the profits for himself. That is, the owner of the cargo tries to ensure the safe passage of the ship. The ships have, for example, hired their own pilots in winter, who are specialized in navigation in ice conditions. The condition of the ships is therefore a cause for concern, but it cannot be assumed that in commercial shipping I would deliberately try to cause environmental damage.

Shipping has a long tradition of free shipping. Coastal states are allowed to inspect ships that arrive at their ports, but in international waters ships must be allowed to pass in peace. In special areas, such as the Danish straits, an international agreement was made as early as the 1850s, in which it was agreed that the strait should not be closed to merchant ships.

In practice, this principle of free navigation can be violated if the ship appears to be a major threat to the natural environment. For example, the ship’s condition is so bad that it can drift off the channel and into the shallows.

However, the concern about accidents caused by the shadow fleet is justified. Shadow fleet tankers have had accidents around the world. There have been cases, for example, in the Strait of Gibraltar, off Cuba and China, and off the coast of Malaysia and Indonesia.

The effectiveness of sanctions

Unfortunately, the price ceiling set by the G7 countries for the sale of oil does not work. Currently, up to 95 percent of the crude oil transported by Russia has been sold at a price higher than the price ceiling, and it is transported by shadow fleets. So the Shadow Fleet has succeeded to displace sanctions-respecting ships in Russian oil shipments and thus the original sanction no longer works.

In the summer of 2024, the G7 countries have introduced new measures to reduce Russian oil exports. They have started directly sanctioning ships. Several dozen ships have already been put on the sanctions list, which means that they will not receive service in European or G7 ports. This has proven to be a remarkably effective measure, as almost all the vessels sanctioned this year have found themselves in a situation where they cannot get cargo to transport.

Next, it can be seen that in addition to crude oil, natural gas transports are also being sanctioned. As I write this, new regulations sanctioning natural gas ships come into force almost every day. We will continue to monitor how these measures work.

The article was previously published in Finnish in Logistiikkaupseeri on October 31st, 2024.